Weak rates, low volumes and high operational costs continue to plague the freight industry. ACT Research’s recent For-Hire Trucking Index noted that capacity, volume, pricing, productivity, and drivers saw continuing declines in April, with a decrease of nearly 6-10% month-over-month across the categories.

ACT’s indexes are based on surveys of for-hire trucking service providers. Its volume category in April was down around 9% from March, which ACT noted was due to momentary volume shift from the for-hire market to private fleets.

ACT Research

ACT Research

Carter Vieth, research analyst at ACT Research, noted that given private fleets’ cost disadvantage, and lack of incentive for backhauls, "we don’t expect this to last long, and recent Class 8 data suggests private fleet capacity additions are slowing, a welcome sign after an extended downturn.”

Vieth said that his firm believes volumes will improve as private fleets reach productivity limits. “Inflation remains a risk, but retail sales in real terms remain positive and were up 3.0% year-over-year in March. Improved imports and intermodal volumes also bode well for improvement.”

Pricing fell nearly 10% month-over-month, though ACT noted that the next few months will be more significant as bid season heats up. Capacity dipped at 6.5%, which is attributed to challenging for-hire condition, with low rates and higher costs driving declines.

The news comes after a similar report wherein ACT significantly downgraded its forecast on the growth of trailer purchases due to overcapacity of trucks in the market from 2023, low profit margins of publicly traded truckload carriers in Q1, soft peak order season, and increasingly diminished backlogs.

“In Q1, profit margins collapsed to a 14-year low 2.6%,” said Kenny Vieth, ACT president and senior analyst.

[Related: Trailer orders indicates a 'year of transition,' forecast affected by overcapacity]

As for-hire capacity shrank for the past 10 months, and with large fleets lowering capex budgets for 2024, delayed capacity additions are likely to continue.

“Class 8 sales trends suggest the ongoing capacity additions at private fleets, a key reason the downcycle has drawn out so long, are slowing too, reducing overall capacity additions and downward rate pressure," Carter Vieth noted.

Though private fleet competition has weighed on volume the past few months, Carter Vieth noted that it’s likely temporary. “Solid performance of rates and the load/truck ratio in the spot market through Roadcheck suggest the gradually improving volume trends will support the market balance in 2024,” he said.

However, the problem remains that private fleets continue to add capacity in 2024. Although this is shifting and requires time, Carter Vieth noted that cost economics should discourage further additions and encourage freight to the for-hire market.

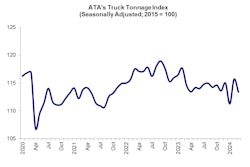

This also aligns with ATA’s Truck Tonnage Index for April, which saw a decline of 1.2% month-over-month and 1.5% from April last year. This is the 14th straight year-over-year decline.

“The truck freight market remained soft in April as seasonally-adjusted volumes fell for the second straight month,” said American Trucking Associations Chief Economist Bob Costello. “With a rebound in freight remaining elusive, it is likely that additional capacity will leave the industry in the face of continued softness in the market.”

Used truck market

For a second straight month in April, pre-owned Class 8 truck retail sales have dropped. ACT’s State of the Industry: U.S. Classes 3-8 Used Trucks saw a 1.9% month-over-month drop to $58,900. Year-over-year basis were 17% lower.

ACT Research

ACT Research

The downward pressure on prices has weakened moderately from Q4 2023 to Q1 2024, said Steve Tam, vice president at ACT Research. “Prices are expected to remain relatively stable through most of 2024, transitioning to year-over-year growth in late Q3 or early Q4. Sequential growth most likely will take place at the end of 2024.”

Talking about volumes, Tam explained that the 5.6% drop was less than the seasonal decline indicated by history. He added that wholesale activity contracted by a much greater amount, down 30% month-over month.

“Predictably for the first month of the quarter, auction sales paled at -48% month-over-month,” he said. “Combined, the total market same dealer sales volume shrank 30% month-over-month in April.”